Intelligent Document Processing for mortgage originators: a real ROI analysis

One of the best ways to uncover AI use cases with a solid return on investment is to see concrete industry-specific examples. In this article we’re walking through the value created by AI-powered intelligent document processing for mortgage originators.

Documentation in mortgage origination

Mortgage originators are banks, credit unions, and non-bank lenders originating residential purchase and refinance loans. Examples include companies like United Wholesale Mortgage, Rocket Mortgage, loanDepot, Pennymac, etc.

With every loan application, W-2s/paystubs, tax returns, bank statements, appraisals, title commitments, closing disclosures, and other document types have to be reviewed and processed. Cost to process a loan doesn’t show up as a single line item. The true cost is found in headcount, processing time, error rates, and the quiet churn of customers who gave up and went somewhere else.

Every year the mortgage industry files public data on origination volume, denial rates, and loan economics. That means we can get visibility into real numbers from real companies, not just hypotheticals. The MBA Quarterly Performance Report and Freddie Mac's Cost to Originate Study give citable, audited benchmarks that many industries don't have publicly available. That’s what we’re using for this exercise.

Understanding the cost of work

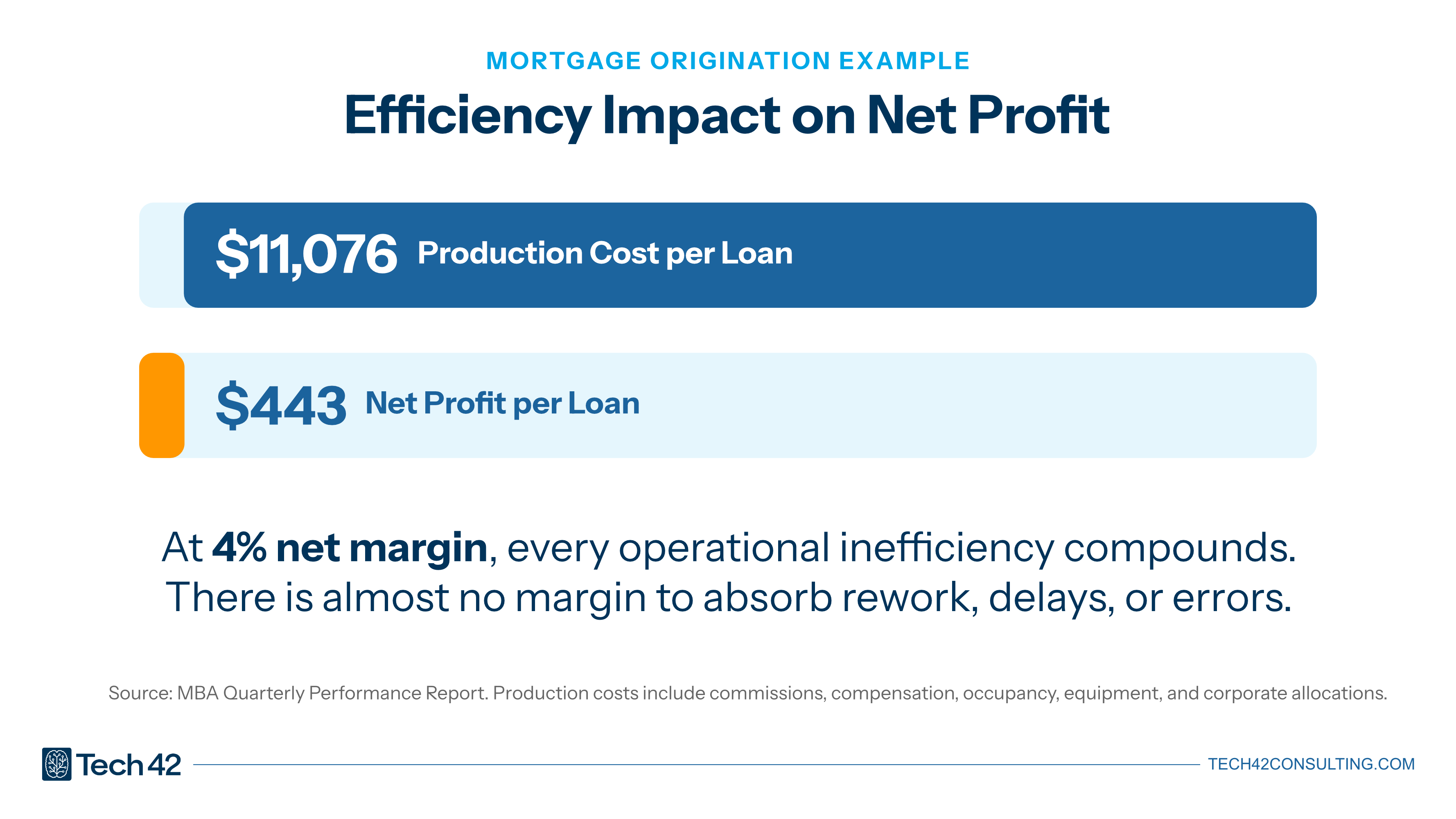

Before we can calculate a return for intelligent document processing, we need to understand the cost of the existing work. In mortgage origination, the MBA reports that “production costs” average $11,076 per originated loan, which includes the cost of “commissions, compensation, occupancy, equipment, and other production expenses and corporate allocations.” Net profit? A lean $443 per loan.

That's a margin so thin that a single operational issue like a rework, a delay, or a file that gets re-touched three times can erase the profit on multiple loans.

Three ways intelligent document processing generates savings for mortgage originators

As we’ve written about, you can think about AI value in terms of both efficiency and opportunity/growth. Let’s walk through three tangible examples of how this plays out.

Per-loan processing costs (efficiency)

This is the straightforward and traditional efficiency play. If you can process work in less time, there’s you spend less in payroll per loan. If you can process work with fewer tools, you can reduce software costs. You get the idea.

For context, Freddie Mac's 2025 Cost to Originate update found that lenders maximizing digital automation save $1,700 per loan and shorten production timelines by an average of five days.

According to the full study, the spread between the most and least efficient lenders makes this concrete: top-quartile lenders average a cost of $6,900 per loan. Bottom-quartile lenders average a cost of $16,500. That $9,600 gap is largely a measure of operational efficiency.

Here’s an example of how the math breaks down:

Formula:

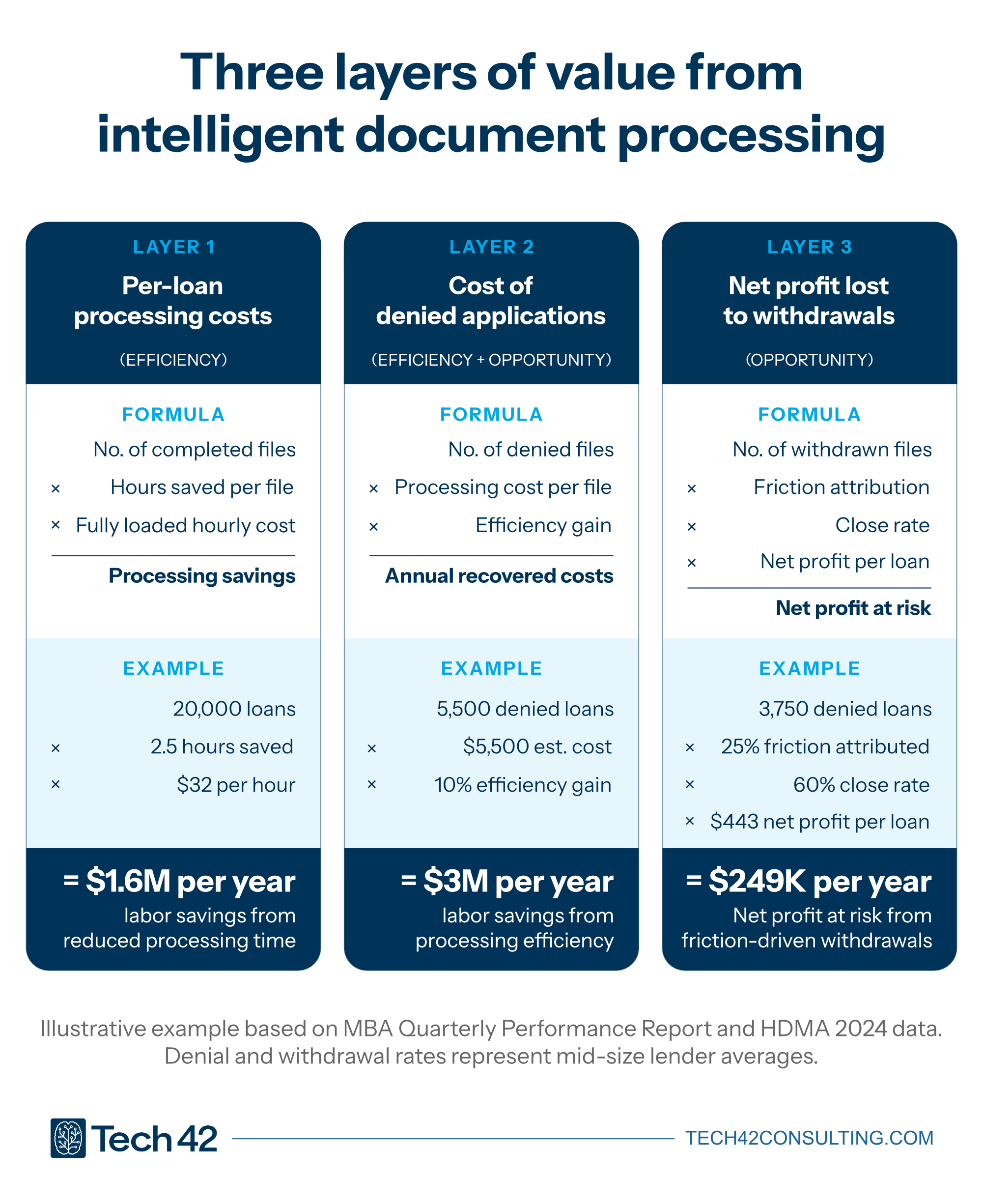

Volume of completed files × Per-file hours saved × Fully loaded hourly cost = Processing savings

Example:

20,000 originated loans × 2.5 hrs saved × $32/hr = $1.6M/year in labor savings

This example doesn’t even get into the increased complexity of other loan types like FHA and VA loans.

Cost of denied loan applications (efficiency + opportunity)

In the mortgage industry, work that doesn’t generate income equates to denied and withdrawn loan applications. A loan that gets denied after a full underwriting review consumes processor time, underwriter time, and document management overhead.

The same dynamic exists in insurance claims that get rejected, legal matters that don't proceed to engagement, or healthcare authorizations that get denied.

At a mid-size lender processing 25,000 applications per year with a 22% denial rate, that's roughly 5,500 files that touched every stage of the workflow and closed nothing. In 2024, the HDMA reported that the average denial rate for mid-size lenders was 16.5% with denial rates reaching as high as 60.3%.

Here’s the estimated cost to a company:

Formula:

Volume of failed files × Processing cost per file = Annual cost of no-output work

Example:

Let’s assume that the processing cost of a denied loan is lower than the full $11,076 of an originated loan since some expenses, like commissions, won’t apply. We’ll use $5,500 as the estimated processing cost of a denied application.

5,500 denied files × $5,500 estimated processing cost = $30.25M in cost with no revenue

Now, imagine the impact of improving your document review efficiency to capture even a 10% efficiency gain: $3M per year.

The real AI question here goes beyond just automation. What if you could identify files that are going to fail, earlier in the process? Every stage of review you eliminate on a non-qualifying application is direct savings. This starts to move you from simple efficiency gains to a competitive advantage by helping you better qualify business before you get too far down the process.

Revenue lost to application withdrawals (opportunity)

Denied loans are clear, but what about withdrawn applications? These borrowers who started the process and stopped. Maybe they abandoned their search, or maybe they went with a competitor.

Continuing our example with mid-size lenders, the HDMA reported that withdrawal rates in 2024 averaged 22.6%, reaching as high as 84%.

How much of this withdrawal is due to friction? Slow document turnaround. Unclear requirements. Long waits with no status update. As an example, Rocket Mortgage claims that they are closing loans 2.5x faster than the industry average with their deployment of AI-driven document processing, directly compressing the window in which customers give up. And increasing the capacity for their team members.

One way to think about the math is revenue:

Formula:

Withdrawn volume × Attribution rate × Close rate × Revenue per closed unit = Revenue at risk

Example:

3,750 withdrawn apps × 25% friction-attributed × 60% close rate × $11,520 revenue = ~$6.48M at risk annually

But a more meaningful way to think about the math is net profit:

Formula:

Withdrawn volume × Attribution rate × Close rate × Net profit per closed unit

Example:

3,750 withdrawn apps × 25% friction-attributed × 60% close rate × $443 revenue = $249K in net profit at risk

And if your net profit per loan increases, this becomes even more valuable.

Estimating the ROI of Intelligent Document Processing

We’ve outlined different aspects of the savings an AI-powered intelligent document processing solution can generate, but system cost is another factor. Some companies will lean toward general SaaS providers, while others (especially in highly regulated industries) may opt for a custom solution in their own, secure cloud environment.

Regardless of your path, factor in up-front implementation cost and any on-going costs for your solution. As an example, we have a calculator to estimate the cost of running IDP solutions in AWS.

It’s not hard to picture an extremely fast ROI in the mortgage industry based on the amount of documentation, process, and cost associated with loan applications. As you translate this example to your own industry, identify the equivalent metrics:

- Cost per [document type] processed/reviewed

- Cost per [document type] denied/rejected

- Denial, rejection, and withdrawal rates

- Time to process complete document workflow

- Capacity per FTE

Then ask what a realistic and meaningful improvement would be. That’s your starting point for evaluating an AI use case that has a specific goal and tangible business impact.

Next steps in AI transformation

Regardless of your industry or current stage in AI adoption, if you’re processing significant volumes of documentation, images, or video, AI-powered IDP can have a significant impact on your bottom line.

We’ve implemented custom IDP workloads that meet the strictest regulatory and security requirements, including HIPAA and SOC-2. If you’re investigating use cases, check out our executive AI workshop, focused on identifying high-value, high-ROI opportunities. And if you’re ready to dive into a detailed IDP discussion, schedule an IDP consultation.

Andrew Thomas